Brian Innes, Executive Director, Soy Canada

Brian Innes, Executive Director, Soy Canada

Pulse Beat 96, Fall/Winter 2022

GLOBAL CONFLICT AND INFLATION have made markets incredibly volatile in 2022. With the Russian invasion of Ukraine sending markets into chaos and many countries still recovering from the impacts of the global pandemic, commodity markets have been on a roller coaster.

Despite volatility, global demand for soybeans remains strong and continues to grow. Decreased production and low ending stocks combined with increased demand for livestock feed in the Middle East, renewed interest in biofuels in the United States and strengthened soy food consumption in Asia and West Europe are all driving soybean demand.

As the world’s fifth largest soybean exporter, Canada is well positioned to help fill this growing demand for both commodity and non-GMO food grade soybeans. Our incredible farmers and a world-leading value chain make us an important supplier of sustainable sources of protein and oil for a hungry world.

Global soybean production levels are expected to increase for the current marketing year (September to August) due to record levels in South America, but Canadian soybean demand is expected to remain strong.

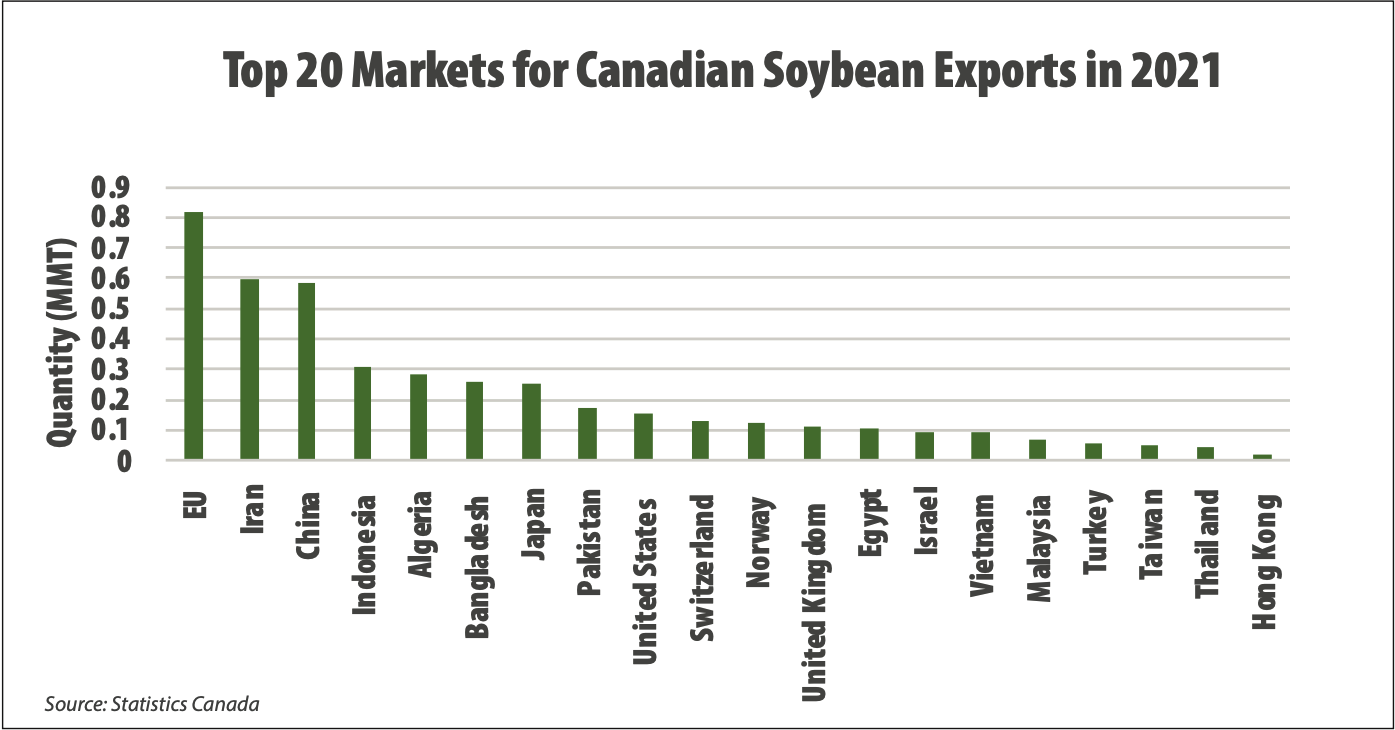

In 2021, Canadian soybean exports were 4.4 million metric tonnes (162 million bushels) representing approximately 70 per cent of production.

Export markets for Canadian soybeans have shifted in recent years. Despite the EU remaining the largest destination for Canadian soybean exports, Iran, Algeria and Bangladesh are seeing growing volumes. Thanks to expanding livestock industries seeking cost-competitive feed options and shifting geopolitics, Canadian exports have seen significant growth to each of the countries.

No understanding of global soybean demand is complete without looking at China, the world’s largest soybean market. Recently, Chinese demand has slowed due to continued COVID restrictions, slow economic growth and a drop in pork consumption. While increased demand is anticipated for the 2022-23 marketing year, import projections remain lower than prior to the pandemic.

Helping to offset lower demand from China is renewed interest in biofuels from the United States, Canada and other developed countries. Leading the way is renewable diesel, a “drop-in” renewable fuel for diesel engines that can be blended at any level with fossil diesel. Significant investment in renewable diesel, which is seen as a solution to reducing greenhouse gas emissions, is taking place due to government regulations that favour low- carbon fuels and major investments by oil companies and private industry.

The market potential for soybean oil as a low-carbon feedstock or renewable diesel is significant. It is causing a major shift in US soybean demand and an unprecedented expansion of soybean processing capacity. It is estimated that renewable diesel capacity in the United States will reach 6.5 billion annual gallons by 2030. This expansion is driving demand for vegetable oils, including soybean oil, and will change the mix of soybeans and soy products available for export from North America as more soybeans are processed on this continent.

RENEWABLE DIESEL CAPACITY IN THE UNITED STATES

Source: Energy Information Administration and CoBank

FOOD-GRADE SOYBEANS

Demand for food-grade soybeans continues to exceed supply as the global soy food industry is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.6 per cent over the next ten years, reaching $73 billion by 2032.

For over 40 years, Canada has been a global leader in producing quality, sustainable food-grade soybeans for international markets. With 1.2 million metric tonnes (44 million bushels) produced each year, virtually all of this production is exported to over 20 different countries around the world.

While exports to traditional markets such as Japan remain stable, significant growth has occurred in new areas such

as Indonesia, creating more demand for Canadian food-grade soybeans. As demand for food-grade soybeans is currently outpacing supply in Canada, there is an opportunity for the country to expand production. Because many varieties are suitable for Manitoba’s diverse growing conditions, from longer to shorter season offerings, the province is well-positioned to help meet this growing demand.

DOMESTIC MARKET

Meat consumption in Canada is on the rise. According to the Organisation for Economic Co-operation and Development (OECD), per capita meat consumption in Canada is increasing annually, especially poultry. Poultry meat consumption in 2016 was 33.3 kilograms and has been increasing continuously, reaching 33.9 kilogramsin 2021. In the past year, meat and livestock exports have remained stable, though hog exports to the United States have been growing due to logistical challenges with domestic processing.

With domestic meat consumption on the rise and export markets holding steady, the Canadian compound feed market is projected to register a CAGR of 3.7 per cent over the next three years, according to a report by Modor Intelligence. As populations increase and income levels rise, meat and livestock exports are increasing, creating more demand for feed ingredients.

WHAT DOES THIS MEAN FOR CANADA?

As populations, income levels and urbanization expand around the world, demand for sustainable feed grains and protein meals from soybeans will continue to grow. Thanks to our incredible farmers and a world-leading value chain, Canada is well-positioned to meet the growing demand for sustainable sources of protein and oil from a hungry world.